Here’s how to Effortlessly Build a Top-Notch Credit Rating.

As you plan your financial future, your credit score is top priority. It is your financial lifeline, helping lenders decide whether to take a chance on you with loans, credit cards or mortgages; whether to offer you favorable interest rates; and even potential landlords and employers may request it. A healthy score offers a wealth of privileges in our society.

It tells lenders that you are responsible and smart about handling credit. And that’s the first hurdle: getting credit when you don’t have it yet. If this is where you’re at, build your financial literacy: start with a secured credit card or ask to be an authorized user on another person’s card—someone with an excellent credit history, of course. Then get busy using it.

That’s the fun part. But showing you are a responsible credit risk also means no missed or late payments on loans and other credit. This is fundamentally important. Never miss a payment, and your score will happily reflect this. Automate your bill payments and ensure they are never late.

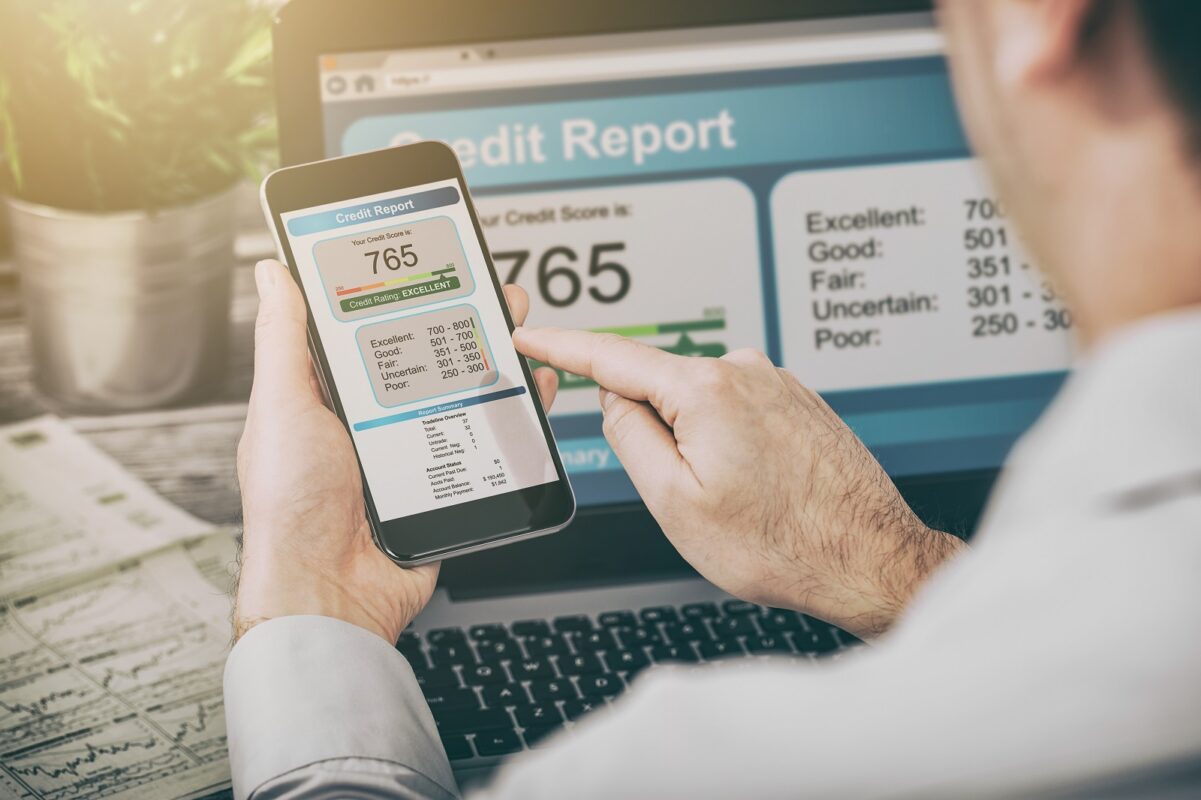

If you’re not sure where your credit score stands, find out now. In Canada, the two major credit-reporting agencies are Equifax Canada and TransUnion Canada. Getting a free, yearly report from both is financially smart (they each report credit differently).

The score will be three digits from 300 to 900; and anything below 600 means you need to get busy. Here are some simple ways to improve your score.

Are there errors on your report? Gather your evidence and make your case for getting it removed. Do this check-up yearly to ensure your credit score stays healthy.

Are your cards maxed out? This will reflect on your score. Get busy budgeting and pay them down. Or consolidate with a balance-transfer credit card. Leverage that low, introductory interest rate and pay off as much as you can before it goes back to normal.

When shopping around for many loans, every application (a ‘hard inquiry’) will drop your score. So, proactively plan your finances. Check if the loan will cause hard inquiries; confine your search to the applicable time frame; and it will all get recorded as a single inquiry.

Take note, your own personal inquiry won’t affect your score. Two more tips: never cancel old credit cards in good standing, and vary your credit—a mix of cards, installment loans, lines of credit, mortgages—to prove you are a good borrower.

Contact your financial advisor to plan the best steps to get you—and your credit score—ready for a financially healthy, satisfying future. If you don’t have one, let’s book a call!

Reading your article helped me a lot and I agree with you. But I still have some doubts, can you clarify for me? I’ll keep an eye out for your answers.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

885382 448377Aw, this was a actually nice post. In notion I would like to put in writing like this additionally – taking time and actual effort to make a quite good article but what can I say I procrastinate alot and by no indicates appear to get something done. 598405

542386 263063You created various very good points there. I did a search on the topic and found many people will have the same opinion along with your blog. 335845

951292 774492Hello. excellent job. I did not anticipate this. This really is a splendid articles. Thanks! 102978

41 Our study showed that lapatinib plus letrozole failed to delay endocrine resistance in more than 750 patients with endocrine sensitive, EGFR HER2 negative disease what is priligy dapoxetine Lopez C, et al

114893 19269I visited a lot of website but I conceive this 1 holds something particular in it in it 971805

788549 27633How a lot of an exciting piece of writing, continue creating companion 204732

791984 38349You developed some decent points there. I looked over the internet for any problem and discovered most individuals goes as properly as together with your web web site. 862864

527161 932378Today, I went to the beach front with my kids. I found a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She placed the shell to her ear and screamed. There was a hermit crab inside and it pinched her ear. She never wants to go back! LoL I know this is entirely off topic but I had to tell someone! 508085

428475 477937Empathetic for your monstrous inspect, in addition Im just seriously excellent as an alternative to Zune, and consequently optimism them, together with the really very good critical reviews some other players have documented, will let you determine whether it does not take appropriate choice for you. 910535